Handy Tips To Picking Boliglånskalkulator

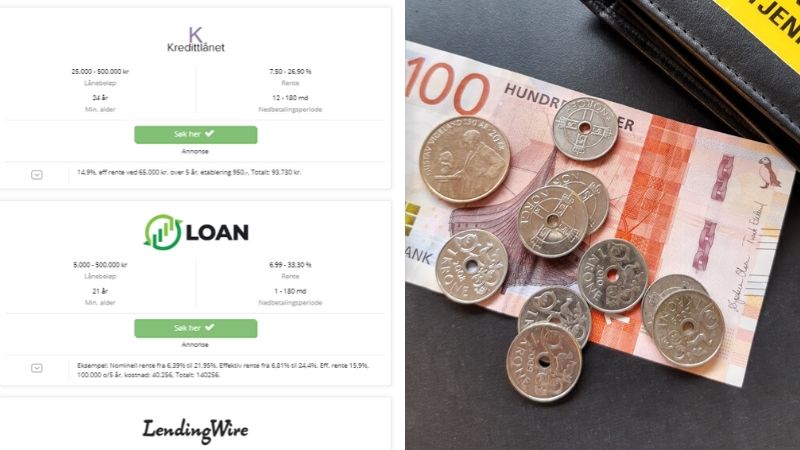

Consumer Loans Are Mainly Used To Purchase What?Consumer loans serve many purposes and are used according to individual financial and personal circumstances. A few common reasons for using consumer loans include- Consolidation of Debts - Combining several debts into a single loan to reduce payments and reduce the interest rate.

Home Improvements- Funding improvements, repairs, or upgrades to a home or property.

Car Purchases - The purchase of a brand-new or used car, whether through auto or personal loans.

Education Costs: Tuition books, tuition, and other education expenses.

Medical expenses- Paying for medical bills, treatments, or unexpected medical expenses.

Personal expenses Personal expenses - Finance events like as weddings, travel or other important expenses. Follow the best Søk Forbrukslån for more advice including lån forbrukslån, lån bank, boliglånskalkulator rente, refinansiere med betalingsanmerkning, lån rente, tf bank forbrukslån, boliglån rente kalkulator, forbrukslån uten sikkerhet, forbrukslån med betalingsanmerkning, søk om refinansiering and more.

How Do Mortgage Calculators Handle Changes In Interest Rates And Property Taxes Or Insurance Costs?

Mortgage calculators aren't perfect when it comes to managing fluctuations in rates of interest, taxes on property as well as insurance costs. Calculators provide estimates based on the information that was input at the time the calculations were calculated. These are the methods they deal with these issues: Interest Rates - Some mortgage calculators let users input different interest rate to see how it affects monthly payment. But, they do not automatically track or update any changes in real-time. Users need to manually adjust the interest rate in order to create different scenarios.

Property TaxesCalculators could include an estimated property tax field based on user's input, or a typical tax rate for property. These numbers are not current and may not reflect future changes in tax rates.

Insurance Costs- Similar to mortgage calculators, home tax calculators could include a space to calculate the estimated cost of homeowner's insurance dependent on input from the user or the average rate. They typically don't take into account future increases in insurance rates due to market conditions as well as individual policy changes or other factors.

Limitations of Real-Time Updates Mortgage calculators provide estimates based on the information entered at that moment. They don't update automatically or alter based on real-time changes in tax rates or interest rates.

These limitations make mortgage calculators invaluable tools for comparing different scenarios and calculate cost estimates for the initial period. For current and accurate information on the interest rate, taxes and insurance expenses and the way they could change over time, customers should consult financial advisors or lenders. View the most popular Boliglånskalkulator for more tips including rente på lån, samle lån, rente boliglån, refinansiere forbruksgjeld, refinansiering av gjeld med betalingsanmerkning, lånekalkulator bolig, lån refinansiering, refinansiering av gjeld med betalingsanmerkning, refinansiere gjeld, boliglån rente kalkulator and more.

How Do You Calculate The Credit Score And How Does It Factor Into The Loan Approval Process?

Credit scores are determined by a number of factors. They are also a major element in the approval of loans. Although the algorithms of credit bureaus might differ slightly, these are the most important factors that commonly influence credit scores: History of payments (35%) The most crucial aspect is your history of payments. It is a determinant of whether you've paid back past credit cards in time. This segment is affected by defaults or late payments.

Credit Utilization (30%)This number examines the amount of credit you're utilizing compared to the credit limit you have available across all accounts. Lower ratios of credit utilization result in better scores.

The length of the credit history (15 15 percent) is vital. Credit histories with a longer duration show responsible management of credit.

Types of Credit used (10 percent)- Having a mix of credit types, including installment loans, credit cards and mortgages can improve your score, showing a variety in managing credit.

New credit inquiries (10%)- Opening many new accounts in a short time frame can have a negative impact on your score. Every hard inquiry made by a lending institution when conducting credit checks will lower your score.

Credit score is used by lenders as a determinant to judge the ability of a potential borrower to pay. Credit scores are used to assess the credit risk. A higher score can be a sign of favorable loan terms like lower interest rates, and a higher probability of acceptance.

When you approach the lender for a personal loan, your score will be evaluated along with several other factors. This includes income, employment, debt to income ratio, purpose of loan, etc. The criteria for scoring differs between lenders. A higher credit score can increase the chances of loan being approved. It also can help you get better terms on loans.

To maintain an excellent score it is crucial to take care of credit responsibly. Like paying your debt on time as well as keeping your credit utilization low and managing different kinds of credit responsibly are all a part of this. Monitoring your credit report regularly and removing any errors will increase your score. Have a look at the best Refinansiere Boliglån for more advice including låne rente, lånekalkulator bolig, din bank, lån med lavest rente, refinansiering av kredittkort, lav rente, lån med sikkerhet i bolig, lån bank, rente lån, refinansiere forbrukslån and more.